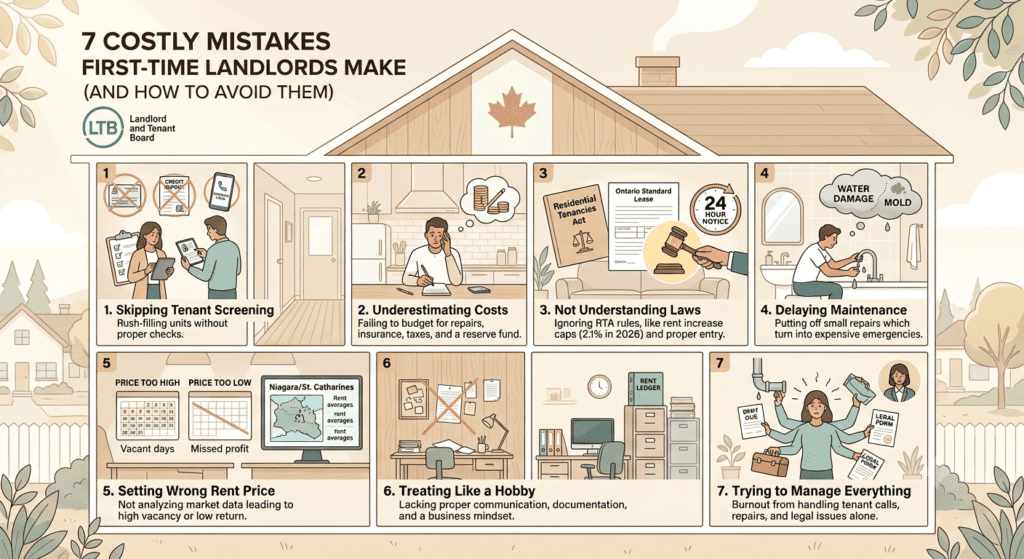

Buying your first rental property feels like a big win. You’ve found a place, run the numbers, and you’re ready to start collecting rent and building long-term wealth. But here’s what nobody tells you at closing: owning the property is the easy part. Running it well is where most first-time landlords make costly mistakes. In fact, many new investors fall into the same traps that can lead to expensive repairs, legal issues, lost rental income, and unnecessary stress. Understanding these 7 costly mistakes first-time landlords make can help you avoid them and protect your investment from day one.

A single bad decision early on, like skipping a credit check, underpricing the unit, or missing a legal notice requirement, can wipe out months of profit. In Ontario, where vacancy rates in regions like Niagara are sitting under 2% and the rules around rent increases and evictions change almost every year, the margin for error is small.

This guide breaks down the seven most common and costly mistakes first-time landlords make, with practical, Canada-specific advice on how to avoid each one. Whether you own a single condo in St. Catharines or you’re managing a long-term rental in Niagara Falls, these lessons will save you time, money, and a lot of stress.

1. Skipping Proper Tenant Screening

This is the mistake that causes the most damage, and it’s almost always preventable. A vacant unit feels like it’s bleeding money every day it sits empty, so new landlords rush to fill it. That urgency is exactly how bad tenants slip through.

Accepting the First Applicant to Avoid Vacancy

When you’re staring down a mortgage payment and an empty unit, the first person who seems “fine” can look like a relief. But a tenant who pays late, damages the unit, or has to be evicted will cost you far more than two or three extra weeks of vacancy ever would. Eviction through Ontario’s Landlord and Tenant Board (LTB) can take months once you factor in filing, scheduling a hearing, and waiting for an order. During that time, you’re often not collecting rent at all.

Not Checking Employment or Income

Pay stubs, an employment letter, or a recent Notice of Assessment tell you whether an applicant can realistically afford the unit. Landlords across Ontario commonly use a benchmark where rent shouldn’t exceed roughly 30 to 35 percent of gross income, but this should be treated as a guideline, not a rigid rule used to disqualify someone outright. The Ontario Human Rights Commission has made clear that a strict rent-to-income ratio used as the sole basis for rejection can amount to discrimination, particularly against applicants relying on social assistance or disability income. The goal is to verify ability to pay, not to penalize the source of that income.

Ignoring Rental History

A quick call to a previous landlord can save you from a tenant who has a pattern of late payments, property damage, or conflict. Ask specific, factual questions: Did they pay on time? Did they give proper notice before leaving? Would you rent to them again? Be cautious of references that come from friends posing as former landlords. Confirming property ownership through municipal tax records is a simple way to verify a reference is legitimate.

Failing to Verify References

Document every reference check, including who you spoke to, when, and what they said. If a dispute ever lands in front of the LTB, this paper trail protects you and shows you ran a fair, consistent process.

Credit and Background Checks Matter

Under Ontario Regulation 290/98, landlords are permitted to request credit checks, credit references, rental history, and income information, but you must get written consent first and apply the same standard to every applicant. As of late 2024, most rental credit checks done through Equifax and TransUnion are treated as soft inquiries, meaning they don’t lower an applicant’s score. This makes it easier to ask for one without putting an unfair burden on renters. Look for patterns rather than a single number: consistent on-time payments, manageable debt levels, and no recent eviction-related judgments are stronger signals than a perfect credit score.

Key takeaway: The wrong tenant can cost far more than a few extra weeks of vacancy. A consistent, documented screening process is your single best protection against lost rent, property damage, and lengthy LTB disputes.

2. Underestimating the True Cost of Owning a Rental Property

New landlords often budget for the mortgage and stop there. That’s where the trouble starts. A rental property has a long list of ongoing costs that don’t show up on a mortgage calculator.

Repairs

Appliances break, faucets leak, and locks wear out. These small, routine repairs add up over a year and need to be budgeted for, not treated as a surprise.

Property Taxes

Property taxes typically rise every year, and in fast-growing regions like Niagara, increases can outpace what you’d expect. If you don’t plan for this, a tax bill increase can quietly eat into your margins.

Insurance

Landlord insurance costs more than standard homeowner’s insurance because it covers loss of rental income, liability, and tenant-related risks. Premiums have also been climbing across Ontario as insurers respond to higher claims and construction costs.

Vacancy Periods

Even in a tight rental market, no property stays occupied 100% of the time. Tenant turnover, cleaning, and re-listing all take time. Niagara’s vacancy rate has hovered near 1.8% recently, which is good news for landlords, but it doesn’t mean zero turnover risk, especially with student or seasonal renters.

Emergency Maintenance

A burst pipe or a failed furnace in January doesn’t wait for a convenient moment. These emergencies are expensive precisely because they’re unplanned, and they tend to happen at the worst possible time.

Capital Improvements

Roofs, HVAC systems, windows, and major structural work eventually need replacing. These aren’t annual costs, but when they hit, they can run into the tens of thousands of dollars.

Why You Need a Reserve Fund

A common rule of thumb is to set aside one to two months of rental income per year purely for maintenance and reserves, separate from your regular operating budget. Relying solely on monthly rent to cover every expense leaves you exposed the moment something unexpected happens. A dedicated reserve fund means a leaking roof becomes a manageable repair instead of a financial crisis.

3. Not Understanding Local Landlord-Tenant Laws

This is where first-time landlords get into the most legal trouble, often without realizing it. Ontario’s Residential Tenancies Act (RTA) governs nearly every part of the landlord-tenant relationship, and the rules are detailed, specific, and enforced through the LTB.

Lease Agreements

Ontario requires the use of a standard lease form for most residential tenancies. Using an outdated template or a lease you found online can leave out required clauses or include terms that aren’t enforceable under the RTA.

Security Deposits

Ontario law only permits a last month’s rent deposit, not a separate damage deposit. Many new landlords don’t realize this and try to collect extra funds for potential damage, which isn’t legal.

Entry Notice Requirements

You can’t simply show up to your own rental property. Landlords must provide proper written notice, generally at least 24 hours, before entering a unit for non-emergency reasons, and the notice must state the reason and the time of entry.

Eviction Rules

Eviction in Ontario is a formal, multi-step legal process, not something a landlord can handle informally. Recent changes are worth knowing about: starting September 21, 2026, the notice period for non-payment of rent under an N4 form shortens from 14 days to 7 days for monthly and yearly tenancies. But a notice is not an eviction order. Landlords still need to file the correct form, attend an LTB hearing if required, and obtain a formal order before a tenant can be removed.

Required Documentation

Keep every lease, notice, rent receipt, and piece of correspondence with tenants. If a dispute ever reaches the LTB, documentation is what protects your case.

Rent Increase Rules You Need to Know

This is one area where the rules change every single year, and it directly affects your bottom line as a first-time landlord. For 2026, the Ontario rent increase guideline is set at 2.1%, the lowest cap in four years, reflecting cooling inflation and the government’s stated goal of protecting tenants from steep increases. This guideline applies to units first occupied on or before November 15, 2018. If your unit was first occupied after that date, it’s exempt from the cap and you can set the increase amount freely, with proper notice. To raise rent, landlords must give at least 90 days’ written notice using the official Form N1, and rent can only be increased once every 12 months for the same tenant. If your costs have risen well beyond what the guideline covers, due to major capital repairs or a significant property tax increase, you can apply to the LTB for an Above Guideline Increase (AGI), though approval isn’t automatic and typically requires documented evidence.

Rental laws vary by province, and even within Ontario, municipalities sometimes layer on additional bylaws around things like indoor temperature standards or short-term rental licensing. Staying current on these requirements isn’t optional. It’s the difference between a smooth tenancy and a costly dispute at the LTB.

4. Delaying Maintenance and Repairs

It’s tempting to put off a repair when it seems minor. A slow drip under the sink, a furnace that’s making a strange noise, a few shingles out of place. But deferred maintenance almost always turns into a bigger, more expensive problem.

Small Repairs Become Major Expenses

A small plumbing leak left unaddressed can lead to water damage, mould, and a repair bill that’s ten times what it would have cost to fix early. The same goes for HVAC systems. Skipping annual servicing might save a few hundred dollars now, but it often leads to a full system failure that costs thousands and leaves your tenant without heat or air conditioning.

Tenant Satisfaction Drops

Tenants notice when maintenance requests are ignored. A frustrated tenant is more likely to break their lease early, withhold rent, or escalate a dispute to the LTB. Responsive maintenance is one of the simplest ways to keep good tenants long-term.

Increased Vacancy Risk

A poorly maintained unit doesn’t just lose the current tenant, it also becomes harder to rent out again. Photos of an outdated kitchen or a stained ceiling will sit on listing sites longer and attract fewer serious applicants.

Protecting Long-Term Property Value

Your rental property is an investment, and like any investment, it needs upkeep to hold its value. A roof that’s properly maintained can last 20 to 25 years. One that’s neglected might need full replacement a decade early. The same logic applies to plumbing, electrical systems, and exterior maintenance.

Best practice: Build a seasonal maintenance checklist (HVAC servicing in spring and fall, gutter cleaning, smoke detector testing, roof inspections) and stick to it. Preventative maintenance is almost always cheaper than emergency repairs.

5. Setting the Wrong Rental Price

Pricing a rental property is part art, part data. Get it wrong in either direction, and it costs you money.

Pricing Too High Causes Longer Vacancies

An overpriced unit sits on the market longer, and every week it’s empty is rent you’ll never recover. Worse, a listing that lingers can signal to prospective tenants that something is wrong with the property, even if the only issue is the price.

Pricing Too Low Reduces Profitability

Underpricing might fill the unit fast, but it leaves money on the table every single month. Over a full year, even a $100 underpricing mistake adds up to $1,200 in lost income.

The Importance of Market Analysis

Pricing should be based on comparable rentals in your specific area, not a guess or a number that simply covers your mortgage. As of mid-2026, average rent across Niagara Falls sits around $1,800 to $1,820 per month, with significant variation by unit type, neighbourhood, and finishes. Smaller markets like Welland and Thorold often rent 12 to 18% below St. Catharines, while basement apartments have seen some of the strongest demand growth in the region, with rents up roughly 9% as renters look for more affordable options. Pulling current comparables from MLS listings, Rentals.ca, or local property management reports gives you a realistic price range instead of a number based on assumptions.

Regular Rent Reviews

Rental markets shift, and your pricing strategy should too. Reviewing comparable rents annually, even if you don’t raise the rent every year, keeps you informed about whether your property is priced competitively. Just remember that if you do increase rent on an existing tenant, you’re bound by the 2.1% guideline and 90-day notice rule covered earlier, unless the unit is exempt.

Practical tip: Price slightly below market for a long-term, reliable tenant if you value occupancy stability over squeezing out every possible dollar. The cost of one month of vacancy often outweighs the benefit of a slightly higher rent.

6. Treating Landlording Like a Side Hobby

Owning one or two rental units can feel casual at first, almost like an extension of homeownership. That mindset is one of the most common reasons first-time landlords run into trouble.

Poor Communication

Tenants who can’t reach their landlord, or who get inconsistent answers, lose trust quickly. That erosion of trust often shows up later as late payments, ignored lease terms, or a tenant who simply stops cooperating.

Missed Documentation

Without a system for tracking leases, notices, repair requests, and payments, details fall through the cracks. And in a dispute, the LTB favours landlords who can produce clear, organized records over those who can’t.

Inconsistent Rent Collection

If rent due dates, late fees, or payment methods aren’t applied consistently across tenants, you open yourself up to claims of unfair treatment, and you make it harder to enforce your own lease terms when it matters.

Emotional Decision-Making

It’s easy to let a tenant slide on a late payment because they had a hard month, or to avoid addressing a lease violation because the conversation feels uncomfortable. But inconsistent enforcement creates problems down the line, both with that tenant and with how confidently you can manage future ones.

Owning rental property is a business, even if it’s just one unit. That means building simple systems: a standard application process, a written maintenance request procedure, a clear rent collection method, and organized digital records. Landlords who treat it this way from day one avoid the chaos that often pushes first-time landlords toward burnout.

7. Trying to Manage Everything Yourself

Self-managing a rental property feels manageable when everything is going well. The cracks show up when life gets busy, or when something goes wrong at an inconvenient time.

Tenant Calls

Maintenance requests, questions about the lease, complaints about a neighbour. These calls don’t stick to business hours, and tenants expect a timely response regardless of when an issue comes up.

Emergency Maintenance

A burst pipe at 11 p.m. doesn’t wait until morning. Self-managing landlords are often the ones fielding these calls personally, coordinating a plumber, and absorbing the stress of an after-hours emergency.

Rent Collection

Chasing late payments, sending reminders, and handling the awkward conversations that come with overdue rent is one of the most time-consuming and uncomfortable parts of self-management.

Inspections

Routine inspections, move-in and move-out walkthroughs, and seasonal property checks all take time and need to be done consistently to protect your investment and your legal position.

Legal Paperwork

From the standard lease to N1 rent increase notices to N4 forms for non-payment, Ontario’s paperwork requirements are detailed and unforgiving of small mistakes. A notice filled out incorrectly, or delivered the wrong way, can delay an entire eviction process by months.

Vendor Coordination

Finding reliable, fairly priced contractors for plumbing, electrical, HVAC, and general repairs takes time to build. Without an established network, self-managing landlords often end up paying more or waiting longer for the same work.

Why Self-Management Becomes Overwhelming

For one unit, self-management is often manageable, especially early on. But as responsibilities pile up, tenant issues, maintenance, legal compliance, rent collection, and vendor coordination, the time commitment grows faster than most first-time landlords expect. This is where a professional property management company becomes valuable, not as a luxury, but as a practical way to protect your investment.

A property manager handles tenant screening, rent collection, maintenance coordination, and compliance with the RTA, freeing you from the day-to-day demands while keeping your property running smoothly. This is particularly valuable for landlords who don’t live near their rental property, who own multiple units, or who simply want rental income without it becoming a second job. Professional management also reduces legal risk, since experienced managers stay current on changing requirements like the 2026 rent guideline or upcoming RTA amendments, something that’s hard to track on your own while juggling a full-time career.

Conclusion

Becoming a landlord is a genuine opportunity to build long-term wealth, but the seven mistakes covered here, from skipping tenant screening to trying to manage everything alone, are exactly what turns that opportunity into a financial headache. The encouraging part is that every one of these mistakes is preventable.

Start with disciplined tenant screening and realistic budgeting for the true cost of ownership. Stay current on Ontario’s landlord-tenant laws, especially rent increase rules and notice requirements, since these change yearly and carry real financial consequences if ignored. Address maintenance proactively instead of reactively, price your rental based on real market data, and run your property like the business it is.

And if the day-to-day demands start to outweigh the benefits, know that you don’t have to handle it all yourself. Treating rental property ownership as a long-term investment means recognizing when professional support adds more value than it costs.

If you’re a first-time landlord in Niagara Falls, St. Catharines, or anywhere across the Niagara Region and you want the income without the stress of self-management, The HAH Developments can help. Our team handles tenant screening, rent collection, maintenance coordination, and full compliance with Ontario’s rental laws, so your property stays protected and profitable. Contact The HAH Developments today for a free consultation on how professional property management can simplify your rental journey.

Frequently Asked Questions

Skipping proper tenant screening is the most costly mistake. Accepting the first applicant without verifying income, rental history, and credit can lead to missed rent payments, property damage, and a lengthy eviction process through the LTB.

A common guideline is one to two months of rental income per year, kept in a separate reserve fund for repairs, emergencies, and capital improvements like roof or HVAC replacement.

The 2026 guideline is 2.1%, the lowest in four years. This applies to units first occupied on or before November 15, 2018. Landlords must give at least 90 days’ written notice using Form N1, and rent can only be raised once every 12 months.

No. Ontario law only permits landlords to collect a last month’s rent deposit. A separate damage deposit is not legally permitted under the Residential Tenancies Act.

The process can take several months once you factor in serving the correct notice, filing with the LTB, waiting for a hearing date, and obtaining an order. Starting September 21, 2026, the N4 non-payment notice period shortens from 14 to 7 days, but the overall process still requires multiple legal steps.

It depends on your time, location, and comfort with hands-on management. Many first-time landlords with full-time jobs, properties in another city, or limited experience with Ontario’s rental laws find that professional management pays for itself through reduced vacancy, fewer legal mistakes, and time saved.